I suppose it was inevitable.

In 2022, family incomes vs inflation a bigger hit than it died in any calendar-year during the housing crisis, the 70s etc…

Given that GDP was a hair positive during that same time mathematically one of two things were bound to happen. Either

a.) record business profits would occur, or

b.) the harsh, worst-since-the-Great-Depression news that was already hitting families would start to hit businesses.

Not surprisingly the economy is on path “b” not path “a.”

From the article

Inflation rebounded in January at the wholesale level, as producer prices rose more than expected to start the year, the Labor Department reported Thursday.

The producer price index, a measure of what raw goods fetch on the open market, rose 0.7% for the month. Economists surveyed by Dow Jones had been looking for an increase of 0.4%

Point is there is plenty of room for libs to climb on board here

(plenty of room to blame Wall St, banks etc…)

The same folks who mis-estimated mortgage bonds and hand a hand in the housing crash, are the same people currently mis-estimating earnings and inflation.

.

.

Okay, that was 25 years ago so, some of them have retired, but you get the picture.

What I can tell you for certain is that for the past 14+ months Wall street consensus estimates have consistently* predicted

– earnings will be higher than they actually are

– inflation will lower than it actually is

– stock prices will be higher than they actually are

I am not talking about one guy or one firm, but a consensus of many working independently.

I am not talking about one time or two times but dozens of times in a repeated pattern.

Most importantly, if these missed estimates were truly random (not caused by bad education or deliberate ignorance etc.) then half the estimates/estimators would be too negative and half would be too positive.

It is statistically improbable that random happenstance causes the “miss” to almost always be on the same side. Should be half on one side. half on the other, and yet, the “misses” are almost always on the same side.

Actually my constant fair is Bloomberg and CNBC.

They are constantly parading a train of guests who overly-optimistic Wall Streeters.

Here is a chart of recent Wall St earnings estimates, their revisions, and the revised revisions. Chart is made by a statistics group that every quarter, dutifully gathers up all the different estimates from the past 3 months and charts them.

Notice

Each of the new estiomates, 1,2, 3 and 4 were lower than the previous one. Each time the consensus was for nice big earning. Eac thie the consensus estimates were too rosey, too happy, too optimistic, and

Despite revising downward and revising downward again and revising downward again the charts all end

After multiple downward revisions, they STILL think we will return to the 2017 “norm.”

We won’t. We will not return to “the 2017 norm” and I will show that momentarily.

Waiting for your thoughts on this first.

Yes and he is still a CNBC analyst.

They keep inviting him back.

as @tnt put it those guys are ratings whores

in the financial community bad news doesn’t sell.

Look at the above chart. Notice that after revising down several times, the Wall St analysts are now begrudgingly saying “Corporate earnings will return to the 2017 boom, and move upward from there.”

That is crazy-optimistic.

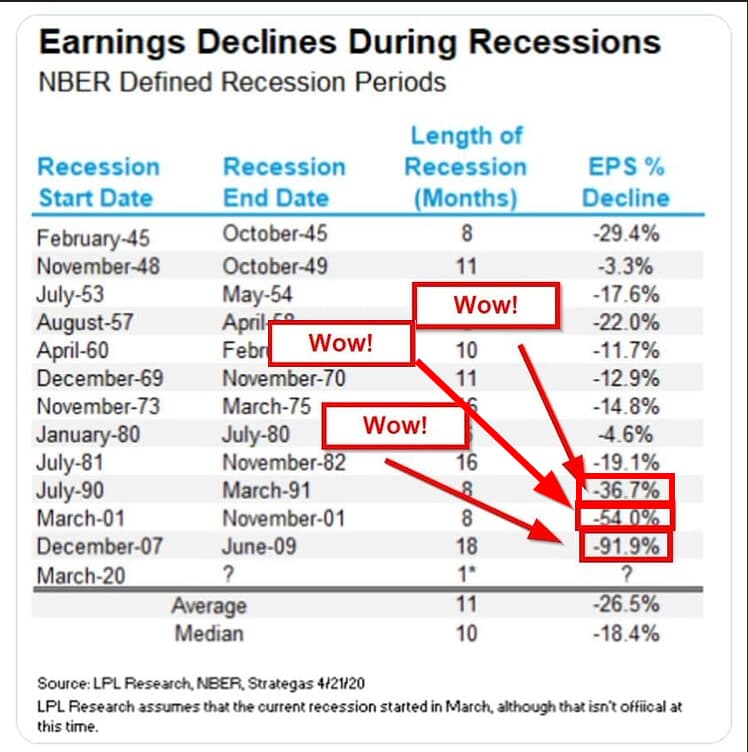

Here is what earnings actually do in actual recessions.

And the Fed has (for different reasons) been making the same whorish forecasts.

Since Oct 22 four months ago

The Fed has “revised” inflation 3 times, each time saying in effect “Whoops we were too dovish. We gave a scenario that was too rosey. We were not concerned enough about inflation.”

The Fed ahs “revised” its interest rate scenario 3 times, each time sayin in effect “Whoops we were too optimistic. We said a low interest rate would fix the problem but it won’t we are going to need a higher rate.”

.