I will go one further.

Already . . .

Already right now it is cheaper to buy a new home than to buy a resale home.

.

.

.

Why? Newly-built homes are smaller and

smaller homes are already what is in demand.

I will go one further.

Already . . .

Already right now it is cheaper to buy a new home than to buy a resale home.

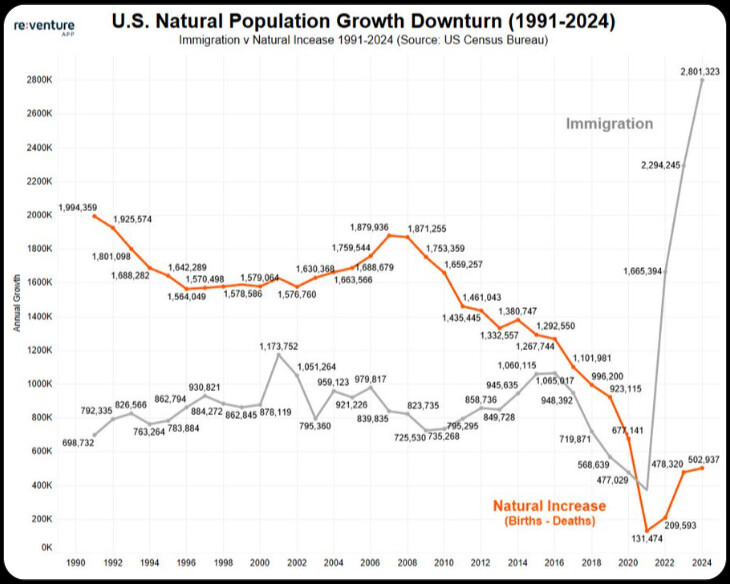

In June 2025, it was roughly 8% or $33,500 cheaper to buy a new house from a builder than to buy an existing house.

This chart is from Reventure a major housing data app (whihc I donpt own).

Reventure’s CEO posted it on twitter with the following comments:

The immigration boom from 2022 to 2024 is hiding a startling fact:

U.S. natural population growth has plummeted.

With growth from Births minus Deaths clocking in at only 502k in 2024.

That’s down about 70% from the mid-2000s.

His 4-part twitter post notes

- I’m also wondering about the rental market and how much it might have been propped up over the last 3 years by the huge deluge of immigration the U.S. experienced.

Various estimates have immigration levels down as much as 95% so far in 2025, so what will that do to apartment demand going forward?

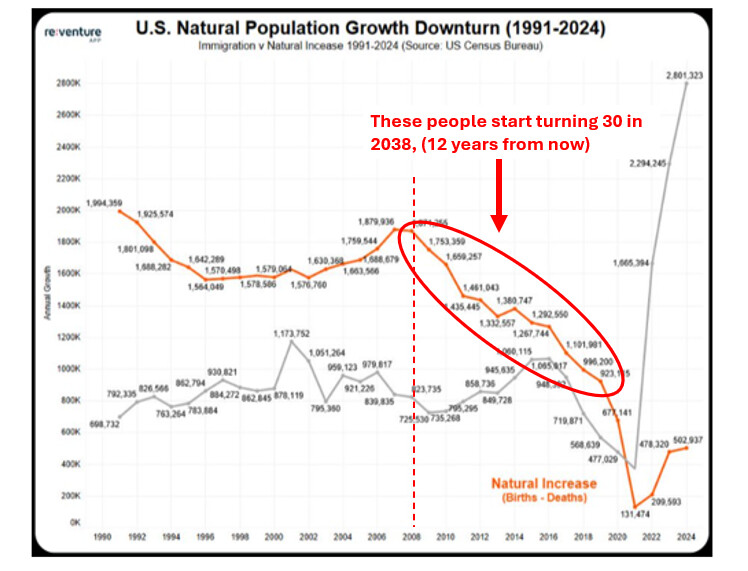

Here are my added notes.

If I have done the math right the market for McMansions will begin a sharp decline 12 years from now.

So . . . no hurry to sell, but I don’t recommend buying one.

.

I disagree. I was able to obtain a 2.86% mortgage. Over the last 13 years, I have averaged almost 7% return on my investments. It makes no sense for me to tie up my wealth in my house.

Mu thoughts have not changed much

bubble likely

if the Fed or anti-free market central planners intervene, (50 year morgtages, transferable mortgages etc) that may spread the pain differently but not make it “less bad.”

the problem with Boomerism is sooner or later you run out of other generation’s money.

+++++

It’s a rhyme

“We don’t know how and we don’t know when, but these two lines will meet again.”

I see all sorts of calls for ending property taxes. It’s a great bumper sticker.

Governments still need the same revenue (unless they cut spending, which they don’t), so they have to get it elsewhere. And they do.

End property taxes for seniors. End property taxes for veterans. End property taxes for all.

Sounds great, but we’re still going to end up paying the same money one way or another.

For the record, I’m not a fan of property taxes. It makes me a captive revenue source unless I sell my home. They can tack on all sorts of extra “fees” and surtaxes, and I really don’t have a say in it. (Oh, look. An extra $7.50 goes to the Library Fund. I though the library was free… Meh. It just comes to 2 cents per day…)

I try to keep an open mind about a general policy of replacing property taxes with something else.

And to ending property tax escrows (when young folks by a house they have to pay a WHOPPING 14 mos taxes in advance into an escrow account).

But

I can understand escrow. Many homeowners don’t have the money to cough up an insurance premium or a tax payment when it is due. When I had a mortgage I resented having to do escrow, but I understood why the lender wanted it. Only back then, it was 3 month of up-front escrow payments, not 14, and then ongoing monthly escrow payments. And lenders paid interest on the escrow balance. (Minimal, but interest nonetheless. Maybe they still do.) A lender doesn’t want the collateral for the loan to go into tax foreclosure or to burn down without insurance covering it.

Ditto that.

I was talking about eliminating property tax in general before, because I see that suggestion a lot. (A guy running for Colorado Governor (a fringe GOP candidate) is calling for that. “Desantis is pushing for it. We should too…” Cool beans (for either state.) But what will replace it?

And as I walk the path to retirement (near term), I certainly benefit from the way Social Security COLAs are structured, and how local property tax breaks cut my property taxes a bit. (It’s not an entire elimination of taxes. It’s a 50% reduction on the first 200K of assessment.) But I agree with you that these structures for Seniors – especially as the life expectancy grows – aren’t smart policy fiscally.

Yes the escrow is not without purpose.

(It serves a purpose)

Nonetheless, it is a VERY large portion of the upfront money buyers need.

I am inclined to support ideas for doing away with it.

But without them you have a tiny Christmas tree.

Yes, yes I do! It’s 6ft tall. ![]()

Imagine, for example, the city of Harrisburg Pa, and the school district each declared

“no property tax will be charege to1st time buyers.”

The tax escrow would then be zero, and at the end of 14 month, it would have 14 mos taxes in the it."

This would keep the lender “safe” and attract a lot of 1st time buyers. (More demand.)

More demand means home values go up. So the current property owners (who do not get to take adantage of it) nonetheless make a gain.

(I presume you’re talking about just bypassing taxes the first year.)

Yes, on the tax escrow front. And to be blunt, it’s the same principle a lot of municipalities offer businesses to move there. (Often multiple years tax-free.) I doubt insurance companies would play along though. But even at that, there could be a special one-year’s-worth of premium added to the mortgage balance to fund the insurance escrow, and then ongoing escrow payments would keep the fund fully funded.

You’re right. Especially for first-time buyers. They’re lucky to scrape together a meager 5% down payment. And then they get told, “Fools! You need twice that much so you can also fund your escrow up front!”

Yes. That is what I am talking about.

“Municipalities (and school districts) could simply decide, 'We will neither charge nor collect taxes on 1st time homeowners during their 1st 14 months.”

The buyer would make the regular payments into the escrow and at the end of 14 months and, at the end of 14 months, the fund is built up completely.

I don’t think it would cost much. Certainly a LOT less than giving blanket tax breaks to seniors or whatever. Only a tiny portion of homes are bought and sold each year (3-4% according to Copilot), and only a fraction of those are to 1st time buyers.

.

.

.

There are other ways.

According to the FHA, fewer than 1 in 400 homeowners (0.25%) lose their homes to foreclosure.

What is the average tax bill for 1st time buyers? About $2,400/year?

0.25% of $2,400 is only $6 a year.

There has GOT to be a cheaper, more efficient way of covering something that costs MBS buyers only (on average) $6 per year per first-time home buyer.

Hannity Community

The official community forum of Sean Hannity. Join the conversation with fellow conservatives on the issues that matter most.